EDITORIAL COMMENT : Reforms to rein in forex cartels

Economic reform was moved up by several big steps at the beginning of this week: the determined two-pronged effort to make the interbank foreign currency mark work as planned, the cut in what amounts to subsidies on fuel, the direct application of a far smaller subsidy on public buses for the ordinary people, the strong steps to stop export earners and their bankers playing the currency markets, and the willingness to vary excise duties to make markets work.

Along with the continued emphasis on fundamentals, and in particular a determination to continue surplus budgeting and keep money supply basically constant or growing very slowly, the measures will go a long way in defeating economic manipulators and others who gain with a crashing exchange rate and high inflation. In fact, there is now a good chance that very soon monthly inflation rates will sink to very low rates and might even go negative as corrections move through the system.

While bus fares and fuel prices have hogged the headlines, easily the most crucial set of steps were the determined combined and co-ordinated assault by the monetary and fiscal authorities on the manipulators and cartels that were rigging the foreign currency markets. The February Monetary Policy Statement had set up an interbank market for the roughly half of export earnings the exporters were allowed to retain in nostro accounts. But that market never really took off. It is known that most banks were less than enthusiastic and that exporters, often with the connivance of their bankers, instead wanted one-on-one deals with importers using what they called the parallel market rate, but what is in fact, a rate set on pavements around Eastgate for US dollar banknotes, in effect letting vendors set monetary policy.

This vendor rate is easy to manipulate by those using that market to skim currency and profits, with the worst manipulation seen last week, when the vendor rate soared. It is such a small market, basically a fraction of Diaspora money coming in via Western Union, that even modest blocks on RTGS dollars pushed into the market, or for that matter pulled out, can move the rate up or down by more than 50 percent.

The result of the manipulations and the reluctance to enforce rules, saw the accumulated retained export earnings mounting in nostro accounts, with reports suggesting that the total was approaching $1 billion, a figure that explains why the interbank market was being starved. Banks were regrettably abetting the market bypass in two ways: they were prepared to lend money to exporters to cover immediate needs, a business whose profits would rise even more when the inevitable interest rises kick in, and they were cooperative in helping for significant commissions to arrange exporter-importer deals, the sort of arrangement whereby a gold miner will buy raw materials at a very stiff mark-up for a plastic manufacturer.

The reply by the authorities, largely predicted by those who use logic rather than bar rumour to make decisions, was decisive. First the authorities announced that they had a pool of US$500 million to enter the interbank market. That alone pushed down the vendor rate significantly, providing extra evidence that it was being manipulated.

Secondly banks are now barred from arranging the cosy importer-exporter deals. Exporters are supposed to sell their surplus forex on the interbank market and importers are supposed to use that market to access required currency. Everyone generally agrees that forex liquidity is high enough and effective RTGS liquidity low enough to create a market rate well below the vendor rate. Banks still make their fee, but it is much lower than with private deals and the banks have to work at getting their rates right. The next step might well be to bar exporters from paying for imports that have no connection in kind or volume for their own business.

The $500 million intervention sum is a big enough block of cash to hammer the market into shape.

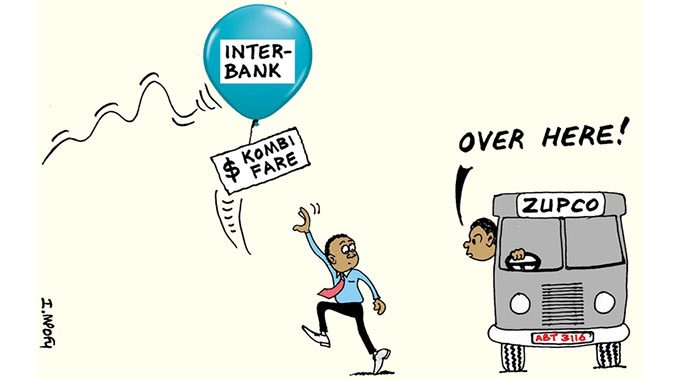

The second set of reform advances concern fuel and subsidies. All Zimbabwean motorists were being subsidised by the unsustainable rate oil companies were being offered US dollars. And by all we mean all, the lady with the S Class Mercedes Benz and the man on the kombi, except that as always with across the board subsidies, the rich benefited the most. That subsidy is now over and oil companies must buy on the interbank market, a market that the authorities are making work. The resultant rise in fuel prices has been partially offset by a decision to halve duty on fuel, reversing a significant part of the December duty rise. The Treasury is still collecting quite large taxes on fuel however, so continues to balance its budgets.

At the same time a targeted subsidy, allowing Zupco to halve bus fares, is being put in place to aid the less well off. The sums allocated to that subsidy are far lower than the value of the forex rate subsidy to oil companies, so cutting the subsidy and quasi-subsidy bill. To be fully effective that move also requires Zupco to expand its fleet, but even with its present minority position in the public-transport market it has enough punch that kombi fares were still at Monday levels yesterday, having fallen to normal last week, after a jump the week before.

You Might Also Like

-

ADDRESSING the nation yesterday from Murambinda B High School, the centre of the national celebrations of the 44th anniversary of Independence, President Mnangagwa, while acknowledging the severe drought this year, was upbeat and positive about Zimbabwe and how it is coping. The drought, the most severe for 40 years and basically the worst in the […]

Agriculture Journal

Comments